Effective August 1, 2024, the CBBC factor is set at 6.25.

The Contribution Based Benefit Cap (CBBC) is a tool SERS began using on August 1, 2024, to identify and prevent pension spiking, also known as benefit inflation. While this is uncommon at SERS, when it does occur, the pension fund must subsidize those benefits. This creates an imbalance for the majority of members whose career salary and contributions followed a normal trajectory.

Benefit inflation can occur when a member’s highest three years of salary are significantly higher than the rest of their career earnings. This results in a traditional pension calculation that is significantly higher than what is supported by their career contributions. The CBBC is fair for all members and ensures that a member’s career contributions support their pension benefit.

The CBBC calculation is separate from the traditional pension formula calculation and is focused solely on a member’s career contribution history. It does NOT change or affect the Final Average Salary (FAS) calculation, which is the average of the highest three years of salary used in the traditional formula calculation.

The CBBC implementation does NOT affect anyone with a retirement effective date before August 1, 2024. The CBBC will NOT be applied to a disability conversion retirement allowance that is capped at 45% of the member’s FAS.

Log In or Create an Account

Create or access your account anytime to manage your retirement information in one place.

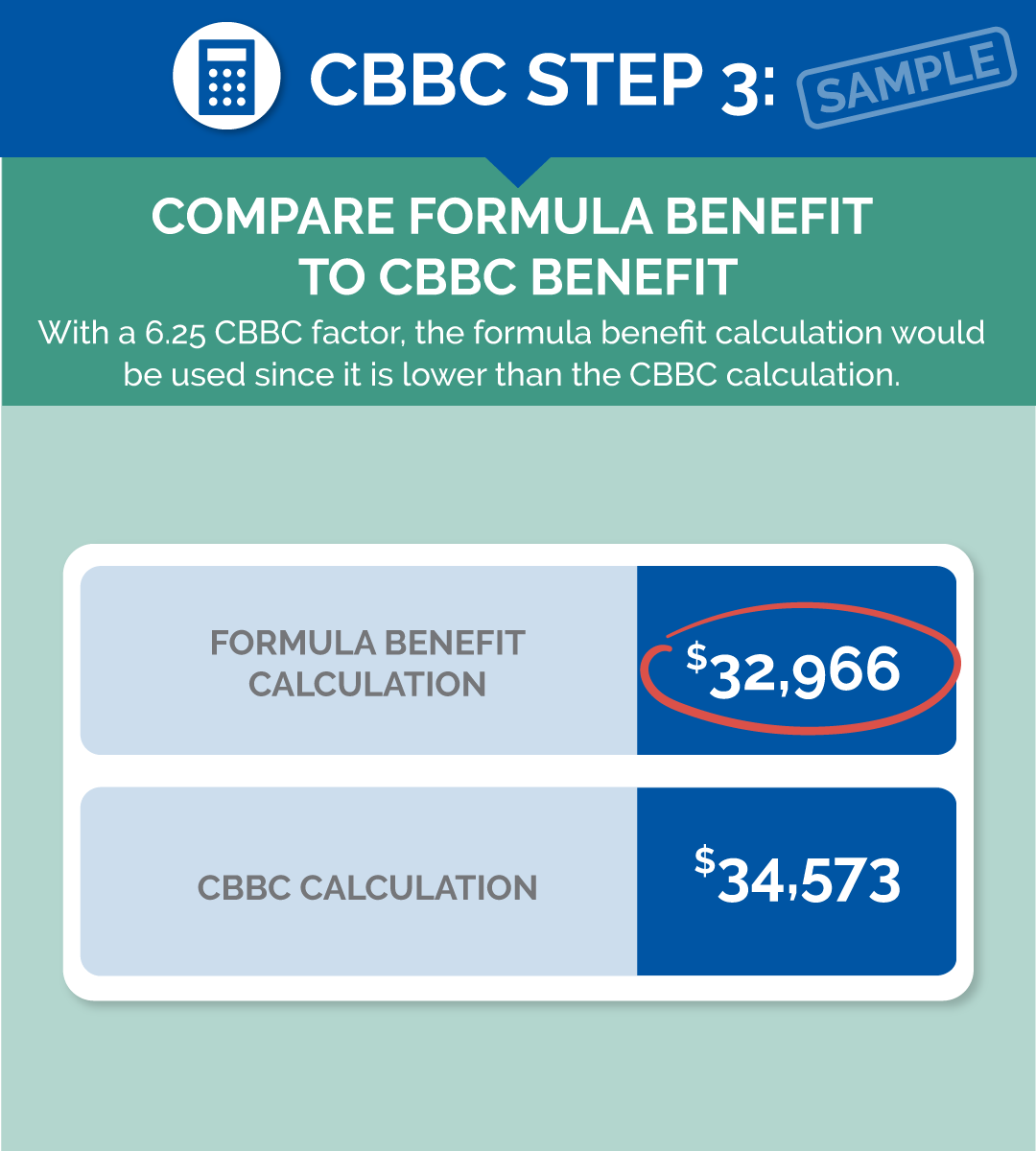

Below, we explain the CBBC calculation and how it will be used. The traditional formula benefit will be used in the majority of pension calculations and only a few situations each year will trigger a CBBC reduction.

To determine if the CBBC will impact you, create a service retirement estimate through Account Login. After entering all required information, review the final estimate screen.

If your benefit is capped by the CBBC, you will see the following message indicating that the CBBC applies. If no message appears, your estimate is not affected based on the information entered.

The monthly benefit amounts shown on this estimate have been capped due to the Contribution Based Benefit Cap (CBBC). SERS cannot project future member contributions or the CBBC factor at a specific retirement date. Estimates based on retirement dates into the future are more likely to indicate a benefit cap. If you continue contributing to SERS, the increase to your member contributions could reduce or remove the CBBC cap. Visit ohsers.forefrontstaging.com/CBBC-explained or contact SERS for more information.

Please note: SERS cannot project future member contributions, so estimates based on retirement dates further into the future are more likely to indicate a benefit cap. If you continue contributing to SERS, the increase to your member contributions could lessen or remove the CBBC.

In most cases, the traditional pension formula will determine a member’s benefit. Only a small number of retirements each year are expected to trigger a CBBC reduction.

The examples below illustrate how different career patterns may influence a member’s personal CBBC factor.

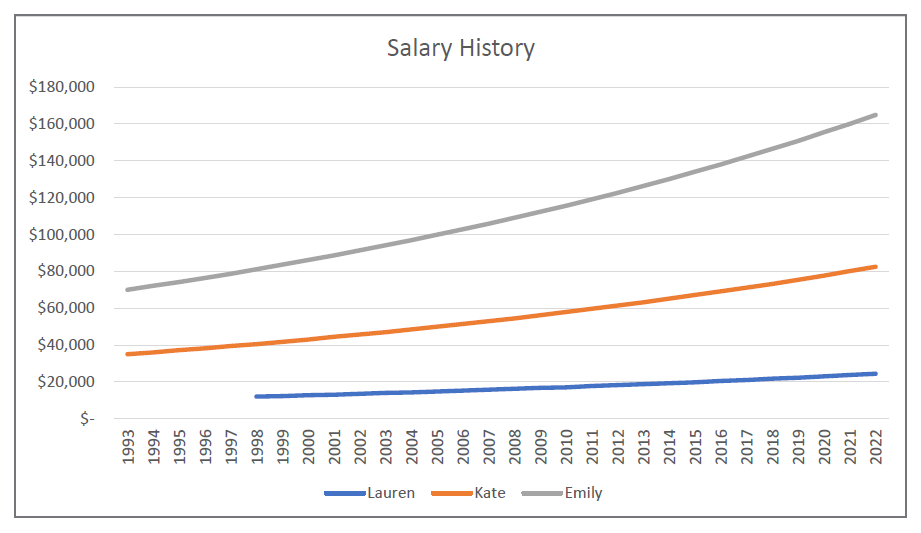

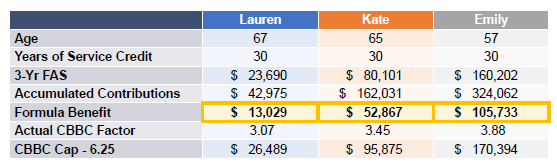

Three members with different salaries all received consistent annual salary increases of 3% over 25 to 30 years. Members with normal salary increases adequately contribute toward their formula benefit. Members should consider their age at retirement, as younger retirement ages can lead to incremental increases in their CBBC factor.

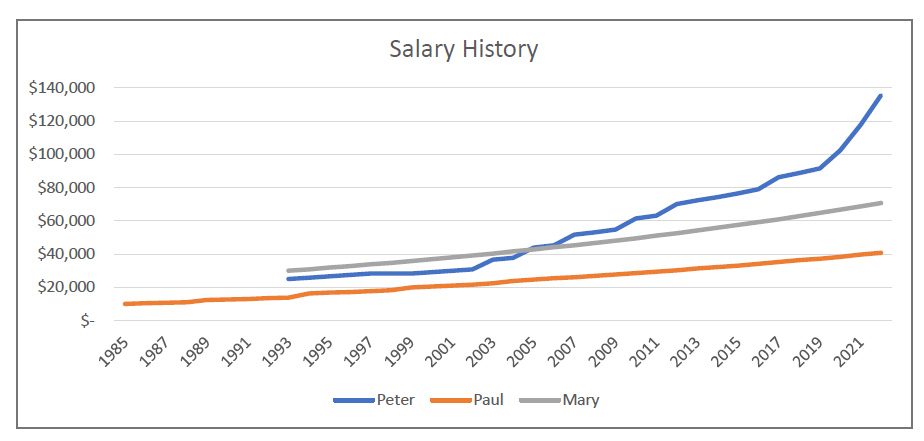

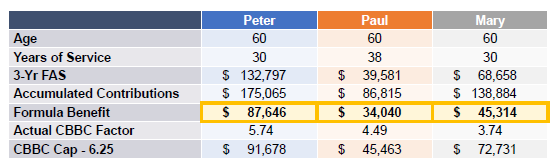

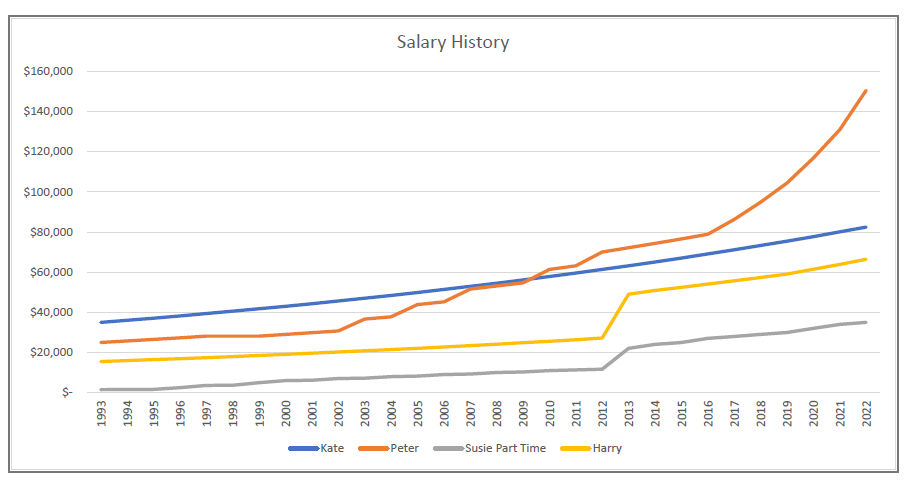

Peter’s 30-year career includes periods of steady increases, no increases, various bonuses, and above-market salary increases near the end. Paul has a 38-year career with steady increases. Mary has a shorter career with steady increases. Although Peter’s late-career raises increased his CBBC factor, his benefit would not be capped at a factor of 6.25.

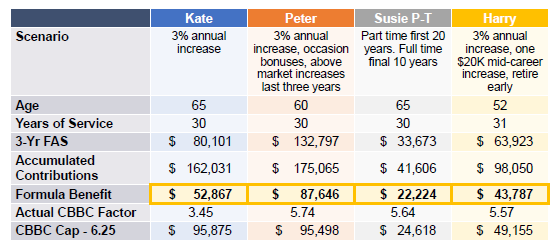

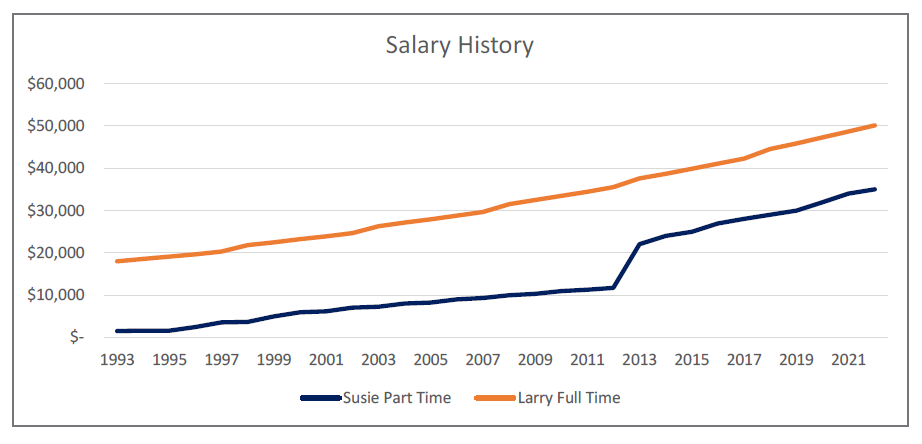

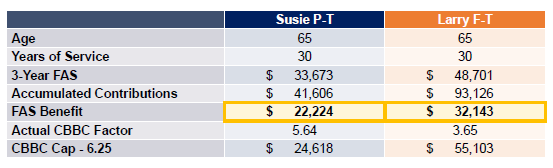

Susie worked part time while her children were in school, then switched to full time. Larry worked full time throughout his career with normal salary increases. While Susie’s transition to full-time work during her final 10 years increased her CBBC factor, her benefit would not be capped at a factor of 6.25.

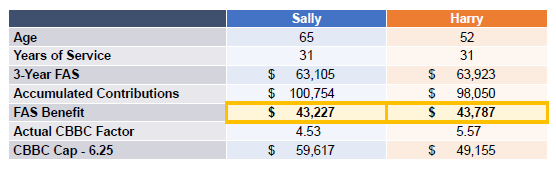

Sally began her career at age 35; Harry started at age 22. Both worked 31 years with similar salaries. Harry retired at age 52 under grandfathered eligibility rules. Because Harry retired younger, his contributions would be paid over a longer period, resulting in a higher personal CBBC factor — however, his benefit would not be capped at a factor of 6.25.

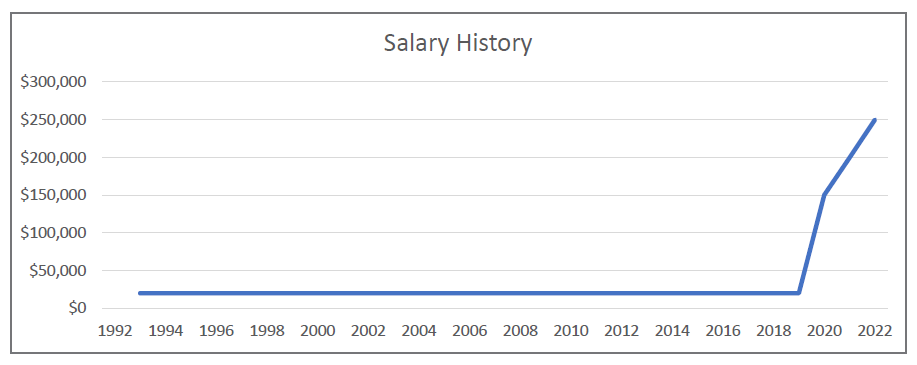

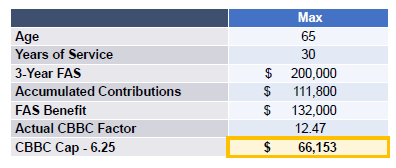

Max earned in the low to mid-$20,000 range for his first 27 years, followed by a significant increase to a quarter-million dollars during his final three years. This results in a formula benefit that exceeds his accumulated contributions in one year. The CBBC ensures Max’s benefit is more consistent with his earnings history. This is the scenario that triggers a CBBC reduction.

A member’s CBBC factor may be influenced by several factors, including the timing of bonuses, above-market salary increases, part-time work, and/or career changes. These factors may individually or collectively affect a member’s formula benefit.

While several of these scenarios resulted in elevated personal CBBC factors, none of them exceed a CBBC of 6.25. Only the egregious salary increases included in the Late Career Salary Boost scenario produced a CBBC factor greater than 6 for the scenarios included in this analysis.

You can view your most up-to-date accumulated contributions by logging in to Account Log In. From the Member Account screen, your accumulated contributions appear under Total Account Balance.

The CBBC determination followed years of thorough discussion and careful analysis by SERS’ Board of Trustees. Materials that assisted the Board in its decision are available in the Downloads section below.

We’re glad you’re a member of SERS. If you have questions about your retirement account or benefits, we are here to help.