Retirement with SERS is a matter of eligibility. To qualify for a monthly, lifetime pension, you must meet specific age and service credit requirements. Eligibility for SERS retirement is separate from eligibility for Social Security, and the two programs follow different rules.

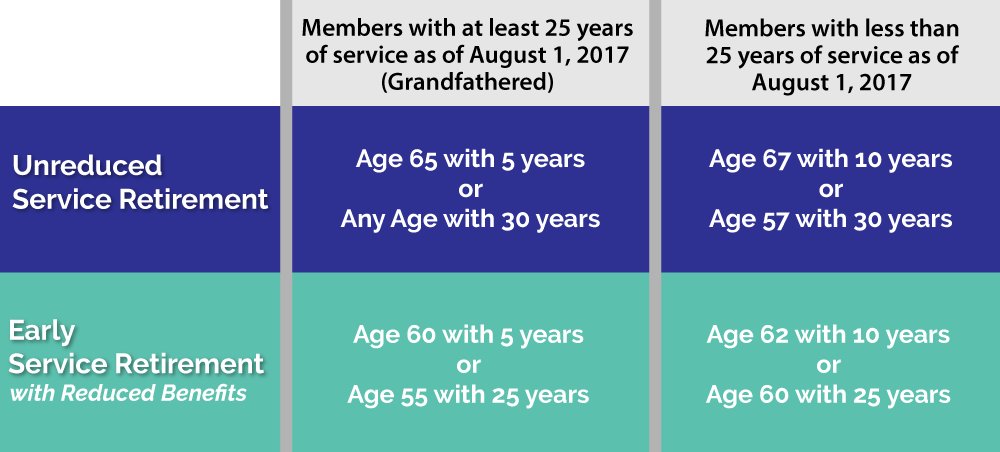

SERS offers two types of service retirement: unreduced service retirement and early service retirement with reduced benefits. With unreduced service retirement, you receive the maximum pension amount available to you. This amount is based on your total service credit, which reflects how long you worked in an Ohio public service job, and your final average salary, which is the average of your three highest years of earnings.

Early service retirement will be reduced to cover the cost of providing a pension over a longer period of time.

Create or access your account anytime to manage your retirement information in one place.

To qualify for a SERS pension, you must meet specific age and service credit requirements. SERS offers unreduced service retirement and early service retirement with reduced benefits.

Your effective date of retirement is the date your pension officially begins. The earliest possible effective date is the first day of the month following the later of:

Your last day of paid SERS-covered employment, or

The date you meet the required age and service credit combination

Choosing the right retirement date matters. Even a short delay can affect your monthly benefit, eligibility for health care coverage, and the timing of your first payment.

Age + Service Credit + Salary = Pension

Your SERS pension is calculated using three factors:

In some cases, delaying retirement by a short period, such as retiring after a birthday, may increase your pension. However, delaying also means giving up one or more pension payments. Comparing estimates for different retirement dates can help you decide which option makes the most sense.

All service credit must be purchased before your retirement date. Our Member Services staff can show you the pension amount before and after purchase of credit. In some situations, you can recover the cost of a purchase in two or three years by receiving a higher pension amount.

When you apply for retirement, you must select a plan of payment. This decision is important and depends on personal factors, including your health, finances, marital status, and other sources of income. SERS staff can provide estimates and explain the advantages and disadvantages of each plan, but the final decision is yours.

All plans provide a lifetime benefit to you. If you choose a plan that continues payments to a beneficiary after your death, your monthly benefit will be reduced. The amount of the reduction depends on the plan selected and the ages of those involved.

You may change your plan selection within 30 days of your first pension payment. After that, changes are only allowed under limited circumstances, such as marriage, divorce, or the death of a beneficiary.

Regardless of the plan you choose, your pension is for your lifetime. You are guaranteed the return of your employee contributions. If both you and your beneficiary die before your total contributions have been paid out, the remaining amount is paid to your estate.

Choosing a Joint Life Plan (Plans A, C, D, or F) may allow eligible beneficiaries to continue health care coverage after your death. Only your spouse and children may qualify for SERS’ health care coverage. Other beneficiaries may receive pension payments, but not health care benefits.

Health care premiums are deducted from monthly pension payments. Upon your death, eligible beneficiaries can continue to receive SERS’ health care coverage as long as they pay the premiums. SERS reserves the right to change or discontinue any health plan or program. For more information, please see the Dependent Coverage section in the Member Health Care Guide.

SERS offers six retirement plans. Each provides a lifetime benefit to you. Plans that continue payments to a beneficiary after your death will result in a reduced monthly benefit. SERS’ staff can provide estimates for each plan.

Provides a lifetime benefit to your spouse equal to half of your monthly pension after your death.

Pays the highest monthly benefit to you, but ends at your death. Any unrecovered employee contributions are paid in a lump sum to your designated beneficiary. If you designate multiple beneficiaries, the amount will be distributed equally among them.

Allows you to designate a specific dollar amount or percentage to be paid to your beneficiary for life. This cannot exceed what you received; if a dollar amount is designated, the minimum must be $100 a month. Federal tax law may require a different minimum amount. In this case, the benefit estimate will show the correct minimum amount allowable.

Pays your beneficiary the same monthly amount you were receiving at the time of death. Due to federal tax law, if there is too great a difference in age between you and your beneficiary (other than your spouse), this plan may not be available.

Guarantees beneficiary protection for a limited period (such as 5, 10, or 15 years). The gross monthly amount to your beneficiary is the same amount you were receiving at death. Beneficiary protection is guaranteed for the period of time chosen, and begins with your effective date of retirement. This plan cannot be changed after retirement.

Allows up to four beneficiaries to receive monthly benefits. Each additional beneficiary reduces your own pension. You must designate a percentage of your monthly pension OR flat dollar amount for each beneficiary. The amount designated cannot be less than 10% unless required by a court order, and the amount for all beneficiaries cannot exceed 100%.

To retire and begin receiving a monthly pension, you must submit a Service Retirement Application. The application must be complete, signed by you, and signed by your spouse if spousal consent is required. You will also need to include any required supporting documents.

Submit your application at least 90 days before your intended retirement date to avoid delays.

At retirement, you may choose to receive part of your pension as a one-time lump sum through a PLOP. This option permanently reduces your lifetime monthly pension.

PLOP payments are typically issued 60 to 90 days after your effective retirement date once all required information is received.

Without a PLOP amount: $780.31

With a PLOP:

|

PLOP

|

PLOP

|

Reduced |

| 6 | $4,681.86 | $745.12 |

| 36 | $28,091.16 | $569.18 |

If you are married and choose a plan of payment other than Plan A or Plan D (with your spouse as beneficiary), or select a PLOP, written spousal consent is required. This must be completed on the Service Retirement Application and signed before a notary public or SERS employee.

If consent is not provided, SERS will pay you according to the Plan A monthly amount. You must advise us in writing if your spouse will not sign the consent.

The spousal consent requirement may be waived if your spouse’s whereabouts are unknown, if he or she is medically unable to give consent, or if a guardianship has been established for your spouse. Your retirement cannot be processed until SERS receives the signed spousal consent, you have notified us that your spouse will not give consent, or until the appropriate document in support of waiver has been filed.

You can apply in two ways:

If you indicated you may be eligible to purchase additional service credit, SERS will mail you a cost statement. All service credit purchases must be completed before your effective retirement date.

Once SERS receives your application:

Your employer must certify your final contributions and last date of service. Each school district has its own policy regarding severance packages for retiring employees.

Before your first payment: Submit a written notice cancelling your initial application, then submit a revised Service Retirement Application with your new selections.

After your first payment: Return the payment, submit a signed written notice cancelling your initial application within 30 days of the initial payment date, then submit a revised Service Retirement Application with your new selections.

If you die before the effective date of your retirement, your retirement will not take effect. Your account will be processed as if you died while still employed, which may qualify your survivors for survivor benefits.

Planning for retirement doesn’t happen all at once. These ten steps are designed to help SERS members think through the key areas that can support a more secure and confident retirement.

Your SERS pension is based on your service credit, highest three years of earnings, and age at retirement. In many cases, working longer results in a higher monthly benefit. Request multiple estimates to compare retirement dates and choose the option that works best for you.

If you’ve worked in other public employment or contributed to another Ohio retirement system, you may be able to combine that service credit with your SERS account. Military service or previously refunded service credit may also be eligible for purchase, which could increase your pension.

It’s important to start saving and have a savings plan in place. Participate in annual programs like America Saves Week to learn more about preparing for retirement.

Tracking expenses, creating a budget, and planning ahead for major purchases can help you reduce financial stress both now and in retirement. Pay off as much debt as possible so you have fewer expenses in retirement.

Planning ahead can protect you and your loved ones. Taking time to create or update estate documents such as a will, trust, or power of attorney helps ensure your wishes are known and your affairs are handled as intended.

Staying healthy supports your quality of life and may reduce medical costs in retirement. Choose physical activities you enjoy, schedule regular checkups, and take advantage of preventive care. Health care needs and coverage often change at retirement. Understanding how your health care options may change, and when to apply, can help you avoid gaps in coverage and plan for future costs.

While working members typically receive coverage through their employer, retirees may be eligible for SERS’ health care coverage based on service credit and other requirements. Premiums, enrollment timing, and available plans can differ significantly from active employment coverage.

Your SERS pension gives you a foundation, but you need more than one income source. Social Security and personal savings can help support your lifestyle, and incorporating other income streams, such as investments and Ohio Deferred Compensation, boosts your overall security in retirement. Ohio Deferred Compensation offers retirement savings options designed specifically for public employees.

Think about how you want to spend your days in retirement. Whether that includes travel, hobbies, volunteering, or part-time work, planning ahead can help you align your finances and goals with the lifestyle you envision. Ask us about being a reemployed retiree.

When is the best time for you to retire? It’s a personal choice based on your budget, beneficiary, and health care needs. We’re here to provide you with information on the options available.

Once your retirement is processed, you will receive a verification letter and begin receiving monthly pension payments. Here is what to expect.

You may be eligible to receive an estimated retirement payment if SERS receives the following at least 30 days before your effective retirement date:

Your estimated retirement allowance is based on payroll and service credit information reported through your most recently completed fiscal year (July 1 through June 30).

Once your employer reports all final pay figures, SERS will finalize your monthly retirement allowance and notify you of the final amount. If the final calculation is greater than the estimated payment, you will receive an additional payment to cover the difference.

If you select a Partial Lump Sum Option Payment (PLOP), it will not be issued until SERS receives all required information from your employer. Please note that this process may take 60 to 90 days after your effective retirement date.

After your initial payment, your retirement allowance is paid on the first of every month. The January payment is deposited on the first business day following January 1.

SERS sends a bi-annual Retiree Focus publication in January and July that includes a statement showing:

You also will receive a statement if there are any changes to your monthly payment amount.

You can view detailed payment information through Account Login.

The Payments section allows you to:

Members who begin receiving benefits on or after April 1, 2018, must wait until their fourth benefit anniversary to become eligible for a cost-of-living adjustment.

When COLA benefits resume, increases are based on the June-to-June change in the Consumer Price Index (CPI-W), with a cap of 2.5% and a floor of 0%.

When contacting SERS by mail, please include your full name and either:

The last four digits of your Social Security number, or

Your full SERS Member ID

It is important to keep your contact information up to date. Even if your benefit is paid by direct deposit, SERS must have your current home address on file. You can update your address easily through the My Profile section of Account Login.

You should also notify SERS when circumstances change, such as:

The death of a spouse who was covered under your SERS health care plan

Changes related to a Joint Life plan of payment

In certain situations, such as a hospital stay or long-term care, you may need someone you trust to act on your behalf. If you want another person to manage matters related to your SERS retirement, you must provide SERS with either a General Power of Attorney or a Limited Power of Attorney.

This is necessary because SERS pension payments may only be handled by authorized individuals. To grant another person authority to manage your retirement benefits, the retiree must either grant Power of Attorney to someone, or a probate court must appoint a guardian for the retiree. A Limited Power of Attorney form is available upon request from SERS. Filing this form also allows the designated individual to update the mailing address for your retirement payments, if needed.

If a retiree becomes unable to manage financial matters and has not designated a Power of Attorney, a probate court may appoint a guardian. A copy of the appointment of the guardian must be filed with SERS to ensure payments are processed correctly and sent to the appropriate individual or address.

A portion of your SERS retirement allowance may be subject to federal and state income taxes. When your pension is calculated, SERS determines which portions are taxable and non-taxable. This information is provided when your first pension payment is processed.

Federal Income Tax

SERS is required to withhold federal income tax from your monthly pension unless you elect otherwise in writing.

You need to file an IRS Form W-4P with SERS to indicate whether we should withhold income taxes. If you do not file this form, SERS withholds federal income tax as if you filed married with three exemptions.

State Income Tax

Your SERS pension may also be subject to state or local income taxes, depending on where you live.

For Ohio residents:

You should consult a tax advisor, the IRS, or state or local tax departments for advice on your specific tax questions. SERS cannot provide individual tax advice.

Both federal and state tax withholding can be updated at any time through Account Login.

Each year, SERS issues an IRS Form 1099-R by January 31 for the prior calendar year. This form shows:

Along with the form, you will receive a SERS Income Tax Information handout that explains the form, and provides other detailed federal and state tax information.

Your 1099-R will also be available in your secure online account by the end of January.

You will receive identification cards from your health plan carrier about 10 days before your coverage becomes effective.

If you enroll in the VSP vision plan, please note that VSP does not issue ID cards. VSP providers confirm benefit information when you schedule an appointment.

If your ID cards do not arrive by your effective date and you need medical services, contact SERS for assistance.

Your original SERS pension is not reduced during reemployment as long as you wait two months after your effective retirement date before returning to a public sector job. If you return to a public sector position before two full months have passed, you will forfeit pension payments for those two months only. After that period, your full pension resumes.

The only exception applies if you held multiple positions prior to retirement. In that case, you may continue working in the lower-paying position without forfeiting pension payments.

Additional rules to know:

Any new benefit earned during reemployment is paid separately as a single life annuity, which you may receive as a lump sum or fixed monthly payments for the rest of your life.

If you return to work after retirement and become eligible for medical and prescription coverage through your new employer, you may temporarily lose eligibility for SERS’ health care coverage. Eligibility is restored once reemployment ends.

Members Who May Be Affected

Members Not Affected

When Health Care Eligibility Is Lost

You may lose SERS health care eligibility if:

* The coverage available to employees in comparable positions must be at the same cost as full-time employees.

You will not lose your SERS’ coverage if:

Regaining Eligibility

Once reemployment ends, your SERS health care eligibility is restored. You have 31 days after losing employer coverage to enroll in SERS’ health care coverage.

Life changes can affect your SERS retirement account. Events such as marriage, the birth or adoption of a child, divorce, or death should be reported to SERS so your records stay accurate and your benefits continue as intended.

If you are single at retirement, select Plan B, and later marry, you may choose a new retirement plan that provides a continuing benefit for your spouse. Likewise, if you were married at retirement, later divorced, selected Plan B, and then remarry, you may change your plan to provide for your new spouse. This change must be made within one year of the marriage. Available plans include A, C, D, or F.

Congratulations on the new addition to your family!

Please sign in to Account Login to update your family and beneficiary records.

Under Ohio law, retirement benefits earned during a marriage are considered marital property that may be divided upon termination of marriage.

If you were married at the time of retirement and elected a joint life retirement plan with your spouse as beneficiary, divorce or dissolution does not automatically change your plan or beneficiary.

Under Ohio Revised Code section 3309.46(E)(2), a retired member may only remove a former spouse as beneficiary with either:

Once the required consent or court order is received, you may update your beneficiary through Account Login.

Upon termination of marriage after retirement, a former spouse is no longer eligible for SERS’ health care coverage. COBRA coverage is available for those who qualify.

For additional details, review the Domestic Relations Guide.

Your future pension payments, including any Partial Lump Sum Option Payment (PLOP), may be subject to an Ohio Division of Property Order that requires you to pay a portion of your pension to a former spouse for purposes of dividing your marital property.

Important details to know:

If you are going through a divorce, you should discuss these matters with an attorney.

If a court orders spousal or child support, SERS may be required to withhold a portion of your pension payments. Even if multiple support orders are received, the total amount withheld cannot exceed 50% of your original pension payment.

In some cases, a court may require you to select a retirement plan that provides a continuing benefit to a former spouse in the event of your death.

For this requirement to apply, the court order must:

If such an order is issued, you must select a plan of payment that complies with the court order.

If your divorce decree includes a DOPO, please send a copy to SERS. You should discuss these matters with your attorney if you are in the process of filing for a divorce.

Your death

Upon your death, a $1,000 lump-sum death benefit will be paid to your designated beneficiary.

If the beneficiary you designated at retirement dies before you, you should name a new beneficiary as soon as possible. This must be done in writing using a SERS form. You may request the form from our office or update your information through Account Login.

If you die early in retirement before recovering all of the employee contributions you made to SERS and selected Plan B (Single Life Allowance), a refund will be issued. Any remaining employee contributions will be paid to your designated beneficiary or your estate.

Death of your spouse

If your spouse dies, the beneficiary structure of your account changes.

Please sign in to Account Login to update your SERS account information promptly.

Death of a beneficiary

If you selected Plan A, C, or D and your beneficiary dies before you, your retirement benefit may be changed to Plan B (Single Life Allowance), with an adjustment to your monthly benefit.

If you selected Plan F and one beneficiary dies before you, your benefit will be recalculated based on the remaining beneficiary or beneficiaries.

We’re glad you’re a member of SERS. If you have questions about your retirement account or benefits, we are here to help.