When you leave a SERS-covered job, you may be eligible to receive a refund of your employee contributions and any amounts you paid to purchase service credit. Employer contributions are not refundable.

Before requesting a refund, it’s important to understand your options and how a refund may affect your future retirement and benefit eligibility.

No Hardship Withdrawals

SERS does not allow partial refunds or loans against your account. A refund of employee contributions is only available after SERS-covered employment has ended.

Account Options After Leaving a SERS Job:

You are not required to take a refund when you leave employment. You may choose to leave your contributions on deposit with SERS.

Keeping your account open has several advantages:

If you return to a SERS-covered job, your account will already be established

You may retain eligibility for disability benefits or survivor protections

If you later work in another Ohio public retirement system, your SERS service credit may be combined for a larger retirement benefit

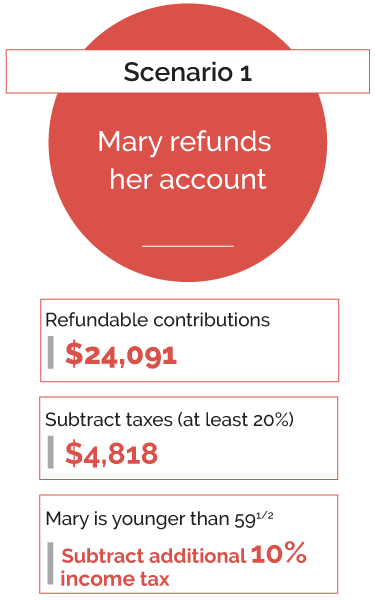

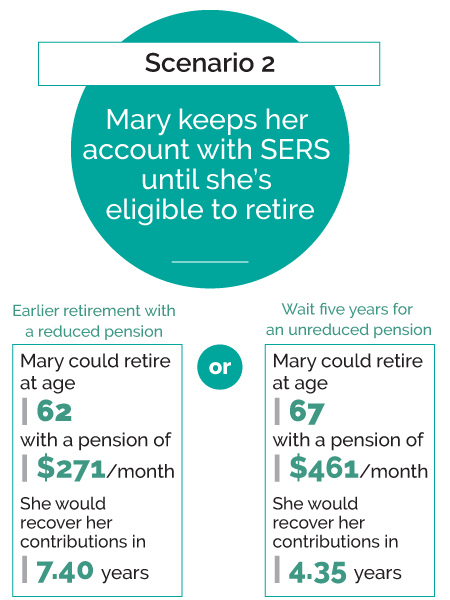

Mary, age 40, leaves her SERS-covered position as a bus driver after 12 years to accept a job covered by Social Security. She may either refund her contributions or leave her account with SERS.

With 12 years of service credit, Mary remains eligible for:

Mary’s employee contributions total $24,091.

Because Mary is under age 59½, choosing a refund would also result in an additional 10% federal income tax for early distribution, unless the funds are rolled over into an eligible retirement account.

To request a refund, you must complete an Active Member Refund Application.

Key points to know:

If you are eligible for an age and service retirement, spousal consent is required before a refund can be processed.

If you are also a member of STRS or OPERS, you may refund your SERS account without affecting those memberships, unless IRS regulations prohibit a refund due to continued employment with the same public employer with whom your last SERS service was earned.

Refunding your SERS contributions may have tax consequences.

If you do not roll over your refund:

If you roll over your refund into an eligible retirement fund such as an IRA, 403(b) plan, or 457(b) plan:

For more information about these and other tax implications concerning a SERS refund, please read the Special Tax Notice Regarding your SERS Lump Sum Payment.

A refund may be subject to:

Support withholding orders

Division of Property Orders (DOPOs)

If applicable, these orders must be satisfied before a refund can be issued.

If you later return to public employment, you may be able to restore refunded SERS service credit.

After earning 1½ years of new service credit with SERS, STRS, OPERS, OP&F, or HPRS, you may restore refunded SERS credit by repaying the refunded amount plus interest.

Payments may be made:

In a lump sum

Through installments

By payroll deduction, if offered by your school employer

Members with an account balance under $5,000 may apply online through Account Login. Once logged into your account, confirm your account balance is less than $5,000 by selecting ‘Member Account.’ When you have confirmed you are eligible to apply online, select ‘Apply for a Refund of Your Account’ to complete an online application.

You will need to provide:

*SERS cannot accept a voided check for a savings account.

If your account balance is $5,000 or more, contact SERS at 1-800-878-5853 to request a Refund Application.

SERS is a qualified governmental plan under IRC Sections 401(a) and 414(d) of the Internal Revenue Code of 1986.

The Internal Revenue Service (IRS) most recently issued a Determination Letter to SERS on May 19, 2017, which was based upon an application SERS filed during the second Cycle E remedial amendment cycle. This Determination Letter does not contain an expiration date. This is consistent with IRS Notice 2016-3’s discussion of Section 21.01(2) of Rev. Proc. 2016-6, which provides that, effective January 4, 2016, determination letters issued to individually designed plans will no longer contain expiration dates.

We’re glad you’re a member of SERS. If you have questions about your retirement account or benefits, we are here to help.